This series is continued from How to File a Roof Hail Damage Insurance Claim.

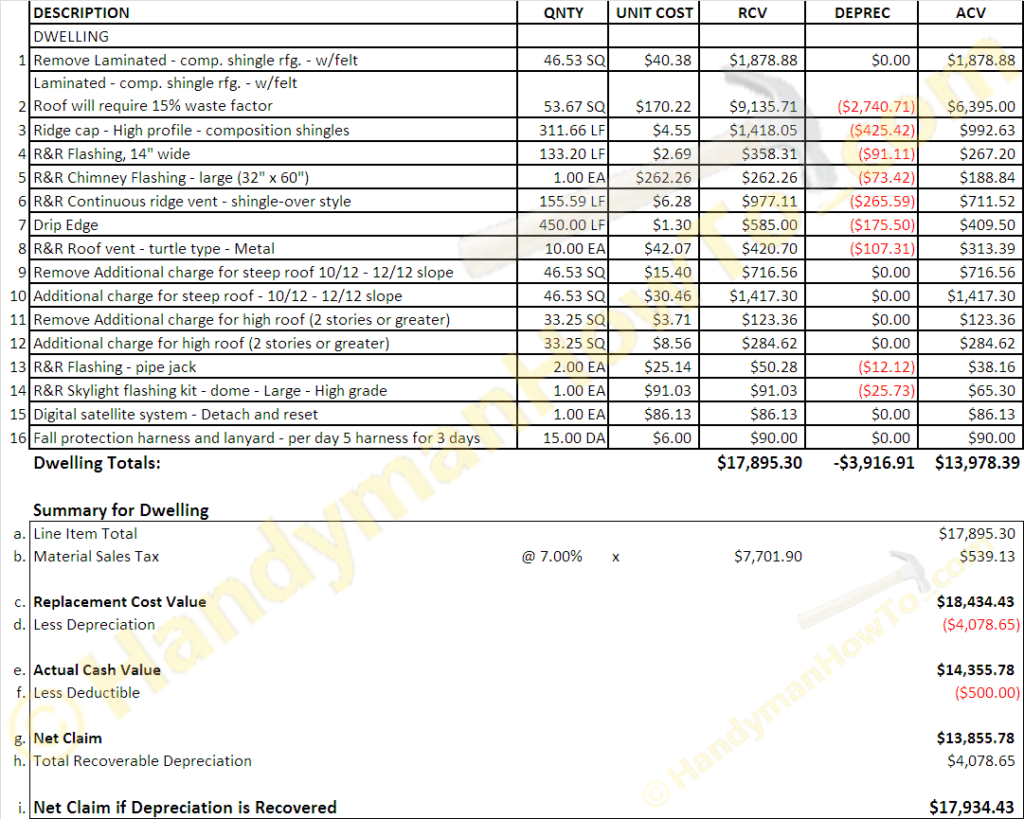

Roof Insurance Adjustment Estimate

The claim examiner approved my insurance claim for hail damage to the asphalt shingle roof. The claim examiner forwarded a copy of the adjuster’s estimate to me which detailed the roof replacement costs for labor and materials. The adjuster’s estimate is a key document that:

- Itemizes the roof replacement costs for labor and materials.

The roofing contractor will use these figures to as the basis for the contract. - Calculates the Replacement Cost Value (RCV), Depreciation (DEPREC) and Actual Cash Value (ACV).

- RCV the full cost of the repair/replacement.

- Depreciation is the decrease in fair value of the roof due to age.

- ACV is the Replacement Cost (RCV) minus Depreciation (DEPREC).

- R&R in the adjustment worksheet means “Remove & Replace”

- SQ means roofing “square” of shingles, equal to 100 square feet area.

- LF means lineal feet.

The claim examiner sent me a check for the Actual Cash Value (ACV) minus my $500 deductible for a Net Claim of $13,855.78, but this falls far short of the $18,434.43 roof replacement cost! What’s going on?!

The difference is the $4,078.65 depreciation (decrease in fair market value) for an 11 year old roof was withheld from the initial claim payment. The reason for withholding the depreciation is some homeowner’s might take the claim check for $13,855.78 and spend it on something other than having the roof repaired. (If you “take the money and run” it can have severe consequences such as having a claim denied for subsequent storm damage that causes the roof to leak and flood the home!)

I made the responsible decision to have my roof replaced which enabled me to file for the recoverable depreciation of $4,078.65 by having the roofing company send a copy of the invoice directly to the claim examiner after the new roof was installed. The insurance company then wrote another check for $4,078.65 for the withheld depreciation. My final out of pocket cost was $500 for the deductible plus $144 to replace three sections of rotted roof deck discovered during the roof replacement.

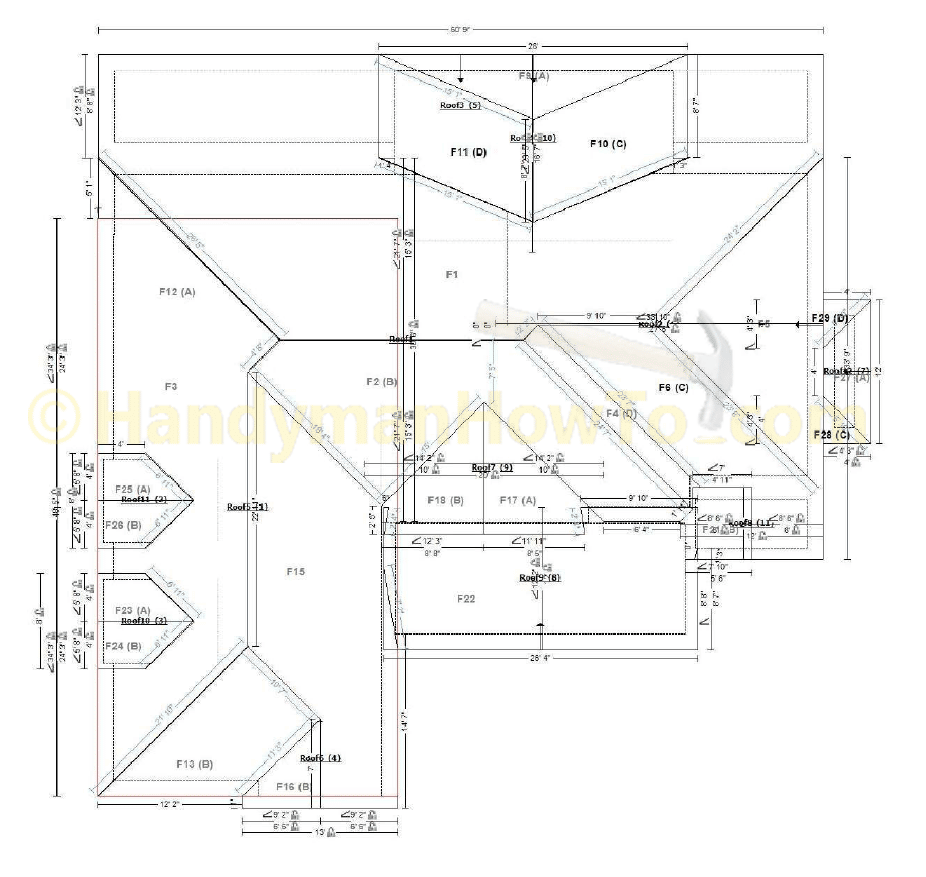

Here’s the roof survey – layout and measurements – that was used to estimate the material and labor costs:

Your roofing contractor will most likely make his own measurements to verify the insurance adjuster’s figures and may order an aerial roof survey as well.

How to Choose a Roofing Contractor

Selecting a roofing contractor is a major decision. A new roof is a “big ticket” purchase and you have to put a lot of trust in the roofing contractor to do the job right because you won’t be able to see what he’s doing on your roof, plus you’re relying on the contractor being in business years from now to back up a 10 year workmanship warranty. Most homeowners won’t to know what to ask for in terms of roofing materials, upgrades and installation details. My goal is to provide you with information to negotiate the best deal and ensure you get a quality job.

The selection criteria and questions you should ask a roofing contractor are:

-

Never hire a roofer that is out-of-state, i.e. “storm chasers”.

They won’t be around for warranty service or dispute resolution. -

Deal only with a factory-certified roofing contractor in your area.

GAF and CertainTeed are the two largest shingle and roofing material manufacturers in the USA.

Find a GAF Master Elite™ or a CertainTeed Premier roofing contractor. -

Check the Better Business Bureau report for your prospective factory-certified roofing contractor.

Avoid roofing contractors with less than an ‘A-‘ rating. A company can be rated an ‘A-‘ minus simply because of the limited length of time in operation, but have an otherwise excellent track record. -

Ask for references from other homeowner’s in your area for jobs within the past year.

Reputable roofing contractors should have dozens and dozens of homeowner’s references. -

Request a copy of the contractor’s professional State license and local business license.

Some States, including Georgia where I live, do not have Professional Licensing requirements for roofers. For example, a plumber in Georgia must pass a State exam to be licensed, but roofer does not. -

Request a copy of the roofing contractors Certificate of Liability Insurance.

Minimum coverage limits should be $1 million General Liability, $1 million Personal Injury and $500,000 for Worker’s Compensation. Higher limits are desirable. Roofing work is dangerous and you don’t want an injured worker suing you or some other accident claim going against your homeowner’s insurance. Call the insurance agency listed on the certificate to verify the policy is in force and the coverage limits are accurate. -

How long has the company been in business?

Roofing contractors tend to come and go due to the ups & downs of the economy and housing cycle. A company that has been in business for many years will tend to be more stable and experienced with adequate cash flow and cash reserves to meet operating requirements.

Dishonest roofing contractors will quickly open & close business under new names (or disappear altogether) in an effort to distance themselves from a poor reputation, unpaid bills and lawsuits. Should the roofing contractor not pay the subcontractor, the subcontractor may file a mechanics lien against your home for the unpaid labor and materials. If this happens, you will not be able to sell your home until the lien is paid. -

Ask if the roofing contractor uses the same work crews and how they train their work crews. Does the company have a training manual?

The workmen on your roof will most always be subcontractors. The busier roofing contractors will be able to retain the same work crews. Visit the company office and ask to see a copy of their roofing manual which sets the standards of competency, workmanship and quality. -

Ask who will be the Job Supervisor.

The job supervisor will be your point of contact for any questions and issues. You should have the supervisor’s business card with cell phone number and e-mail address. The supervisor should be at the job site at least once each day for quality inspections during and after the job is complete.

The supervisor for my roof was there when work began, walked the roof each day, took photos and reviewed the photos and progress with me. When the job was finished, the roofing crew waited for 30 minutes while the supervisor walked the roof, lifting shingles to verify the roofing materials were install correctly. The supervisor had the roofing crew replace a couple of marred shingles in a high traffic area and make a few minor touchups with paint and caulking. The supervisor then reviewed the final photos with me and asked if I had any questions or saw something that needed attention. Only then was the work crew released. -

Ask to see a copy of the roofing contract to read the fine print.

A good contract should include a “Standards of Performance” which states among other things, that the contractor will not nail toe boards through your shingles, kick-outs will be installed at all corners, flashing installation requirements, the crew will not walk or step on your gutters, the job site will be cleaned up at the end of each day, etc. -

How long will it take to replace the roof?

This is seemingly innocuous question can be a red flag. If one roofer says he’ll bring a crew of 15 men and do the job in a day or two at most, while the other roofing contractors says 7 or 8 men will require at least 3 days (weather permitting), immediately disqualify the roofer who says he can do it in a day. Why? Because the roofer with 15 men won’t be focused on quality and will cut corners because he’s in a hurry to finish the job and get paid. 15 men on my roof would be in each others way and they’d probably working well past sunset in the dark. Do you really want that for non-emergency repairs? BTW, my roof required 8 men working for 3-1/2 days to replace the roof – but my roof has complicated lines and features.

Roofing Inspection and Contract Negotiations

You should obtain at least three (3) proposals for your new roof:

- Prepare a short list of qualified roofing contractors per the above selection criteria.

- Contact each contractor and explain that you have an approved insurance claim and are requesting proposals.

- Forward a copy of the insurance adjuster’s estimate to the roofing contractors.

- Make an appointment at your home to review each proposal.

The roofing contractor sales representative will meet with you to walk the roof, check if the insurance adjuster missed anything on the insurance estimate, and go over a contract proposal. Ask questions such that you understand each line item in the contract proposal and how it applies to your roof. Take written notes as necessary.

Thank the sales rep. for his time, explain that you’re comparing proposals from different companies and will make a decision soon. Do not sign anything at this time!

How to Get the Best Roofing Contract

You want to take the best elements from the competing roofing proposals and negotiate with your preferred roofing contractor include it in the revised proposal. Each contract proposal will have unique specifications and insights that you can use to your advantage.

Note that I was NOT negotiating pricing discounts. Why? Because this is an insurance claim for which I plan to recover the depreciation withheld from the Replacement Cost Value (RCV). The roofing company will invoice me for the full $18,434.43 RCV as listed on the insurance adjustment, which I will present to my insurance company for the recoverable deductible. I will also pay the roofing company $500 for my deductible. It would be insurance fraud for the roofing company to give me a kickback, credit, rebate other incentive such as paying my deductible. The State of Georgia passed a Residential Roofing law codified as O.C.G.A. § 33-23-43 which bans these practices.

Since I can’t negotiate a price discount without committing insurance fraud (and a reputable roofing will point out this fact), what I can legally do is negotiate the material, workmanship and warranty specifications. On one hand, the roofer wants to maximize his profit margin by installing less expensive materials and skipping certain installation details to minimize his labor expenses; while I will be negotiating for higher quality items, requiring things be done in particular way, and asking for better warranties that will reduce his profit margin. It’s up to me to do this because insurance adjuster’s report does not go into these details, nor can the insurance company tell me which roofing contractor to hire.

Example roofing specifications that I negotiated were:

- Full replacement of the HVAC flue vents.

- Permanent removal of the attic box vents and installation of new OSB roof deck.

Box vents should not be used with ridge vents due to air flow interference. I had ridge vents installed at my own expense several years before the hail storm. - GAF Timberline® HD™ Lifetime High Definition® Shingles

- GAF StormGuard® Leak Barrier (ice and water shield) over the entire low-pitch porch roof.

- Tear off and replace the HardiPlank® siding on the chimney to apply GAF StormGuard ice & water shield.

- GAF Shingle-Mate® fiberglass reinforced 30 lb roof felt instead of a 15 lb felt.

- GAF TimberTex® Premium Hip and Ridge Cap Shingles from a standard shingle.

- GAF System Plus Warranty (50 years material, 25 years labor).

- 10 Years Workmanship Warranty provided by the roofing contractor.

- New apron/headwall flashing installed where the roof meets a horizontal wall; old aluminum coil flashing to be removed.

What you will be able to negotiate will be highly dependent upon the total value of your roof replacement insurance settlement. The roofing contractor has more room to make concessions on a high dollar job versus a less expensive job. Be polite during your negotiations and mention the competitor included the item in his proposal. Be truthful or you’ll lose credibility because the roofing contractors are all performing the same profit analysis with a “walk away” threshold at which the job is not worth taking. It took me about dozen phone calls and e-mails to work out the final contract terms over a two week period.

Final Roof Replacement Contract Terms

The following are the summary specifications for my hail damage roof replacement contract:

Standard Services:

- Remove 1 layer of shingles

- Remove all felt and debris

- Re-nail and secure loose decking

- Replace rotted, delaminating OSB decking at $48 per repair (not covered by insurance)

- Replace board decking at $2.95 per foot (not covered by insurance)

- Replace rafters at $6 per foot (not covered by insurance)

- Install fiberglass-based deck protector

- Install plumbing vent pipe boots & rain collars

- Paint & seal HVAC vents

- Clean out all gutters

- Clean work site and remove all debris

Additional Options:

- Install new step flashing at all walls, chimneys and skylights

- Advanced Leak Barrier System at: valleys, penetrations, chimney, skylights

- Install ridge vents

- Distinctive hip and ridge caps

- Drip edge flashing

- Warranties:

50 Years Mfg Material Warranty

25 Years Mfg Defect Warranty

10 Years Workmanship Warranty

Notes and Specifications:

The following were line items listed on additional pages in the contract at my request so there was no “wiggle room” in the contract specifications and scope of work:

- Install GAF Timberline® HD Lifetime Architectural shingles – Pewter Gray color

- GAF pro-start starter shingles installed to eaves and rakes

- 10 year workmanship warranty

- Remove tear off, haul, & dispose of existing shingles

- Install GAF ShingleMate® fiberglass deck protector underlayment (comparable to 30lb felt)

- GAF Systems Plus warranty (50 year man. defect, 25 year man. defect labor, 10 year workmanship)

- Install GAF Advanced Leak Barrier® to three (3) dead valleys

- Install GAF Advanced Leak Barrier® to entire deck of 3/12 pitch porch roof (2 year warranty in this section)

- Remove first 4 pieces of siding on 3 sides of chimney and 10 pieces on the south face of chimney, install leak barrier from deck up up the side of chimney box. Re-install and caulk pre-painted HardiPlank® siding.

- Install new flashing at all walls & chimney: install headwall flashing where roof meets wall

- Install new flashing kit for a Solatube sun tunnel skylight

- Install kick outs all corners penetrating roof surface

- Install counter flashing at all stucco walls (BASF SONOLASTIC NP1 will be used to seal top of counter flashing)

- Install white aluminum drip edge to eaves (with no hem) and rakes (with hem)

- Install GAF StormGuard® Leak Barrier at all valleys, chimney, skylight & penetrations

- Install new plumbing boots and storm collars

- Install owner supplied Perma-Boots

- Install new HVAC cap, collar, and flashing kits

- Paint & seal HVAC vent pipes

- Remove box vents and repair related decking

- Remove and replace existing ridge vents

- Remove and re-attach gutter guards

- Remove and reattach satellite dish

- Install GAF Timbertex® hip and ridge shingles

- Blow out / clean gutter system after roof installation

- Clean work site and remove all debris

Deposit and Prepayment

I did not make a deposit, down payment or pre-payment for the new roof replacement contract. Payment in full was due upon completion of the work and I alone was responsible; my insurance company is not a party to the contract.

Before and After Hail Damage Roof Replacement Photos

This is the original 11 year old roof (the roof hail damage can’t be seen from this distance):

The new roof with 50-year GAF Timberline® HD Lifetime Architectural shingles in Pewter Gray color:

Roof and Stucco Wall Flashing Details

The aluminum headwall flashing (where the porch roof meets the wall) was installed before the stucco was applied, then covered with a layer of shingles. The old flashing will be torn and full of holes when the old shingles are removed, therefore the old flashing should not be reused. You can see the aluminum flashing if you look closely below the window on the right.

Apron flashing (also called headwall flashing) is installed on top of the new shingles and against the wall. Black counter-flashing is installed over the apron flashing and sealed with BASF SONOLASTIC NP-1 caulk along the wall:

The next project series illustrates the new roof installation, explaining the details of the roof tear-off and installation process.

Hope this helps,

Bob Jackson